Iran-Linked Hostilities in Iraq and their economic Impact.

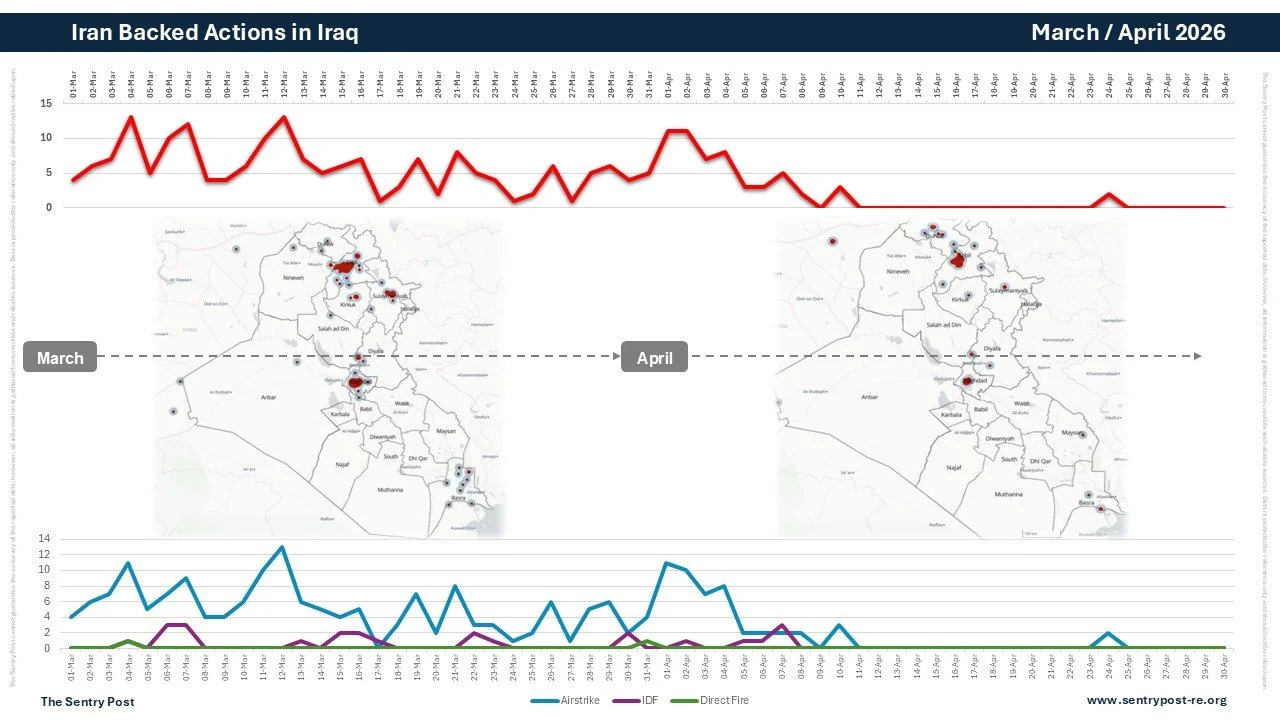

Whilst Iraq has been a primary target for Iranian backed retaliation, there has been a significant downscale in strikes within Iraq from March to April. Total volume of strikes inside Iraq appears to have declined overall with fewer large-scale coordinated attacks and multi-site rocket barrages. Some Iran-backed groups have reduced tempo, likely due to risk of escalation with the U.S., Internal Iraqi political pressure and shifting focus to other theatres (especially Syria). Rather than stopping, Iran-linked groups have changed strategy from frequent, lower-precision harassment attacks to fewer, more deliberate drone/UAV strikes, focusing on symbolic or strategic targets.

A reduction in sustained attacks can create space for institutions in Iraq to function more normally, things like logistics, public services, and supply chains tend to recover quickly when security improves. Ministries and state-linked companies often have contingency plans ready, so even a short period of stability can lead to visible progress in “product delivery” (whether that’s energy, infrastructure, or public services).

Many past de-escalations in Iraq have been temporary. If the underlying political or militia tensions aren’t resolved, institutions may hesitate to fully commit resources. Iraq’s institutional landscape includes federal bodies, regional actors, and non-state groups. Even with fewer attacks, coordination problems can slow recovery. Regional dynamics, particularly involving neighboring countries and allied militias can quickly reverse gains if tensions rise again.

A sustained lull in violence can be an enabling condition for institutional recovery, but it’s not sufficient on its own. The real signal to watch isn’t just the absence of attacks, it’s consistent indicators like: uninterrupted infrastructure projects, stable energy output, timely public sector payments, and renewed private-sector investment.

A US–Iran ceasefire, even a shaky one, feeds into Iraq’s energy sector through a few very specific channels. The effects are real, but uneven and highly dependent on whether the de-escalation actually holds.

Iraq is one of OPEC’s largest producers, so security conditions directly affect output. Fewer attacks (especially on pipelines, export terminals, or foreign operators) make it easier to maintain or slightly increase production. International oil companies tend to resume delayed work, maintenance, drilling, and field expansion, once risk drops even modestly. Production becomes more predictable, but not fully secure.

If the ceasefire collapses, Iraq is one of the first places where proxy escalation shows up (e.g., militia-linked disruptions near southern oil hubs like Basra).

Iraq relies heavily on Iranian natural gas and electricity imports to keep its grid running. This is one of the most immediate and concrete impacts. During tensions, the US often pressures Iraq to reduce these imports via sanctions policy. A ceasefire enables more flexibility for Iraq to continue importing Iranian gas without sudden disruptions. That means a more stable electricity supply (especially in summer), fewer blackouts, and less political pressure domestically. If tensions rise again, gas flows can become a bargaining tool and Iraq’s power grid suffers quickly.

The ceasefire helps Iraq’s energy sector in three practical ways, smoother oil production and exports, more reliable electricity (via Iranian imports), slightly improved investment conditions. But it doesn’t remove the core vulnerability: Iraq’s energy system is still tightly tied to US–Iran relations. As long as that relationship is unresolved, Iraq’s energy sector will keep cycling between fragile stability and sudden risk rather than reaching full reliability.